Collapse: How and When

Collapse: How and When

It’s Not a Matter of “If”

If you prefer the audio of this article, click here.

In our last article on “Dead Internet” we also referred to the “Dead Economy”, where a large part of the global economy, especially that of the West, consists of unproductive or even counterproductive “work”. The radically inefficient nature of these economies has so far been concealed by what amounts to clever accounting, but this is coming to an end.

In this article we are going to explain how the fake economy is coming to an end. And it is going to be uncomfortable. That’s OK. Just bookmark this page and check back in five years. Or maybe two. One caveat: this is an overview, so 1) we will purposefully avoid technical language, and 2) we will be moving very quickly through many concepts that flesh out whole books. We will have something more complete for you on this topic next year.

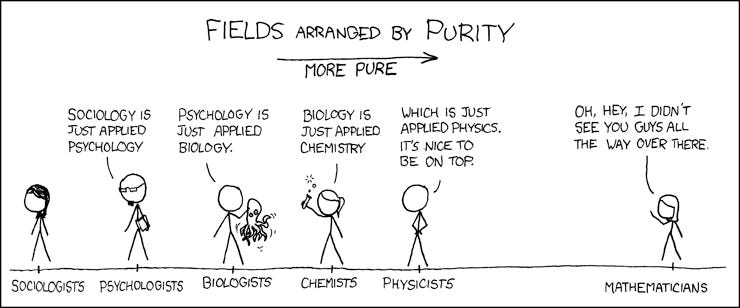

There’s an old XKCD comic worth quoting at this point:

Fig 1. Purity.1

But we could add more disciplines after sociology. Specifically, economics is just applied sociology.

The point of this exercise is that XKCD is right—economics is ultimately just a very rarefied form of physics. There are no major economists in the history of the field that treat it this way, at least not explicitly, though there have been some who recognize it implicitly.2 Economics is a systems science with respect to physics, and physics imposes hard limits. This is unwelcome news for liberalism, which wishes to be free of the constraints of the physical world.3

The detachment of economics from physics has greatly harmed economics as a science. It has blinded it to the fact that the fundamental “currency” of economics is not money, nor value, nor any other such thing. The fundamental currency of economics is energy. No accounting trick will ever produce more calories. The implicit belief that it can, has led us down a very dark path.

In the European Middle Ages, resource management was highly constrained because it was right in front of our face. In those days, wood was the major store of energy, thus the major economic resource. If a community didn’t manage its wood resources, if it deforested its homeland, the community would starve. Because of the relatively low energy density of wood, this process was short-term—it wouldn’t take long to realize that you were running out of “low-hanging fruit”, out of easily accessible lumber, and so naturally, resource management practices arose, along with the social custom of valuing prudence and austerity.

This all changed with the discovery of the New World. Suddenly, an abundance of this energy resource was available. Sure, it was halfway around the world, but in effect it was both infinite and unguarded, and at a large enough scale, it could be shipped back to the motherland at a cost that made sense. All of a sudden, resource management started to fade from view, and the mercantile economy was born.4

The next blow to resource management was the discovery of denser sources of energy: first peat, then coal, then oil. This gave humanity access to stores of energy that would have staggered the medieval mind. And like the lottery winner who no longer has to keep to a budget, Europeans developed a taste for expending this energy. Some of it was well spent; much of it was simply squandered. But the sheer energy density of fossil fuels enabled us to “afford” this expenditure while allowing the economy to grow. There was so much coal around that it was economically efficient just to find more, rather than to spend it thriftily.

In the 1920s, coal production peaked, and we made the transition to an oil-based economy, though not without some bumps in the road.5 Oil was plentiful and denser than any other fuel, so the economy could still maintain efficiency without any real belt tightening. But as oil became less and less accessible, dark clouds started gathering on the horizon. The 1970s saw “stagflation” (inflation with low growth) and oil crises, which gave humanity its first warning signs.

We have been speaking of economic “efficiency” here without saying what this means. Efficiency is really no different in an economic system than it is in a biological system or a physical system. Efficiency is what we call energy return on investment, or EROI. It is the ratio of energy gained from energy expended. For example, a wolf expends energy in finding, hunting, and eating prey. If a wolf uses 500 calories to acquire a deer and gains 5,000 calories from it, the EROI for the wolf is 10. In order to sustain life, individual organisms must have an EROI well above 1.

But due to the second law of thermodynamics, energy is “lossy”—some amount of useable energy (like the caloric energy of food) is always converted into useless energy (like heat). So in a closed system (say, the Earth), EROI is always below 1—we are always losing some amount of total useable energy. Except the Earth is not a closed system because there is an energy input from the sun—the Earth by itself has an EROI above 1, which is how life can be sustained. Every living thing you see on Earth is ultimately “made of” the sun’s energy.

Similarly, we could say that everything in the medieval world was “made of” wood, since wood was the primary store of energy, and today everything is “made of” oil, including green energy. So-called “green” energy sources are just concealed fossil fuels. When you take into account the resources required to extract, manufacture, maintain, and deliver them, they are non-efficient. For an energy source to “break even” requires an EROI of at least 7, which “green” energy sources do not, with the exception of thermal. “Green” energy depends on oil to be viable.6

Since 1970, US conventional oil production has been in decline, which has since been supplemented by LNG, tar sands, shale oil, fracking, etc. However these are much less efficient sources of energy. Since the mastery of oil refinement, the EROI of oil has been declining as oil became harder to find—we were producing more than ever, but also spending proportionally more than ever to get it. In 2018, global crude production peaked. We have now passed what economists call peak oil. It is important to understand that peak oil does not just mean that we’ve hit a peak of wealth that will slowly recede. Since oil is required to get more oil, the inaccessibility of oil has a runaway effect. The less oil we have, the less we can get, and this worsens exponentially.

EROI is the basic measure of the health of the economy as a whole, in the same way that EROI is the basic measure of the success of an organism. A whole economy is much too complex to allow us to measure EROI directly, but we do have an indirect way of measuring it: interest rates.

Interest rates reflect the time-preference of money, or the preference for money now vs. later. Money is just reified energy, and when you borrow money (energy) at interest, you expect to be able to turn that energy into more energy. The interest rate reflects how efficiently you can turn energy now into energy later. If you are highly efficient, you can afford a higher interest rate, which all things being equal, the bank wants to charge. Interest rates are high when lending money is low-risk, and lending money is low-risk when people are productive, or in other words, when they are economically efficient. Interest rates are an indirect measure of economic efficiency—when interest rates are high, EROI is high; when they’re low, EROI is low. Interest rates have declined cyclically since the 1970s, a strong indication that EROI has declined with them.

There are two ways to raise EROI: 1) discover a denser and more exploitable energy source, or 2) use that source in a smarter way. We achieved (1) with the discovery of oil, and we achieved (2) with the discovery of efficient refinement techniques. Neither of these will work today, and that bodes very ill for the future.